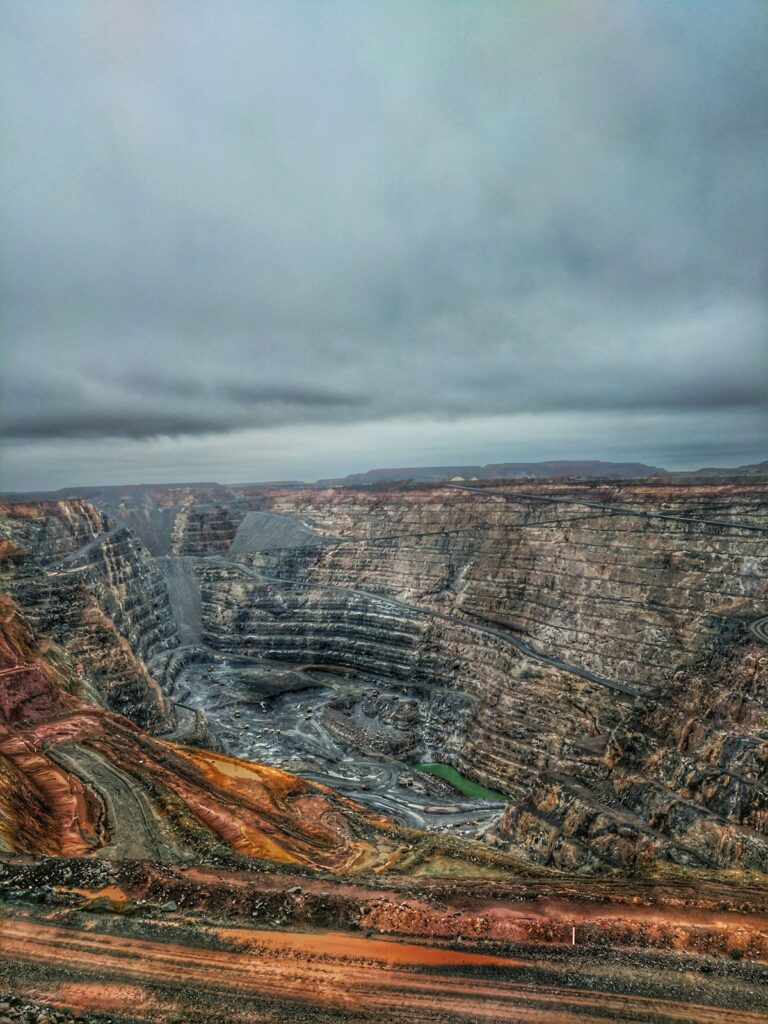

From the cobalt fields of the Democratic Republic of Congo to the copperbelt of Zambia and Zimbabwe’s lithium deposits, Africa finds itself at the centre of a global scramble that it did not choose but cannot afford to ignore. The transition to clean energy technologies — electric vehicles, battery storage, solar panels, wind turbines — has created unprecedented demand for the minerals that underpin those technologies. And Africa, home to the world’s largest known reserves of several of those minerals, is suddenly at the heart of a geopolitical competition that mirrors, in some uncomfortable ways, the colonial resource extraction that the continent experienced a century ago.

The difference this time, African leaders insist, is that the continent intends to participate on its own terms. Across the region, governments are moving to exert greater control over their mineral resources — imposing export restrictions, demanding local processing, and seeking to capture a larger share of the value chain rather than simply exporting raw ore to be refined elsewhere. Zambia recently announced requirements that a significant proportion of copper production be processed domestically before export. Zimbabwe banned the export of unprocessed lithium ore. The DRC, which produces roughly 70 percent of the world’s cobalt, has been locked in negotiations with mining companies over the terms of its mineral development agreements.

The Leverage Question

The critical minerals rush has given African governments a degree of negotiating leverage that they have rarely possessed in previous commodity cycles. Global automakers, battery manufacturers, and technology companies depend on secure supplies of cobalt, lithium, manganese, and nickel — and in many cases, the only viable source is Africa. This has created an opening for African nations to demand better terms: higher royalties, local processing requirements, technology transfer agreements, and infrastructure investments that benefit host communities.

But the leverage is time-limited. The global push to develop alternative mineral sources — including deep-sea mining, synthetic battery chemistries that reduce the need for specific minerals, and new mining operations in non-African countries — means that Africa’s window to extract maximum benefit from its current position may not last indefinitely. “We have a thirty-year opportunity,” said one African minerals analyst based in Johannesburg. “If we don’t use it wisely, we’ll look back and wonder what happened.”

China has been the most aggressive in establishing mineral supply chains across Africa, investing billions in mining operations, processing facilities, and logistics infrastructure throughout the continent. Chinese companies control a significant proportion of cobalt production in the DRC and have invested heavily in copper and nickel operations across southern Africa. The United States and European countries, in response, have launched programmes to develop alternative African supply relationships — but observers note that Western engagement remains less structured and less comprehensive than the Chinese approach.

The Development Paradox

Africa’s mineral wealth creates a paradox that governments are struggling to resolve. On one hand, the global demand for critical minerals offers a genuine opportunity to fund economic transformation — using mineral revenues to build schools, hospitals, roads, and the industrial base that would diversify economies away from raw extraction. On the other hand, the history of African resource wealth suggests that abundance can be as much a curse as a blessing, generating corruption, conflict, and the hollowing out of other productive sectors.

The Democratic Republic of Congo — Africa’s largest cobalt producer and home to significant copper and coltan deposits — illustrates the risks. Despite having mineral wealth that could fund the development of one of Africa’s most prosperous economies, DRC remains one of the world’s poorest nations, its resources captured by a combination of conflict, corruption, and the rapacious practices of both domestic elites and foreign actors. The ongoing conflict in the eastern DRC, in which armed groups compete for control of mining operations and the profits they generate, demonstrates how mineral wealth can perpetuate instability rather than deliver prosperity.

Navigating this paradox requires governance frameworks that most African countries have not yet built. Transparent management of mineral revenues, effective oversight of mining operations, and investment in domestic capacity — rather than simply extracting maximum rent from foreign operators — demands political will that is often in short supply. But the countries that manage to get it right have the potential to use the critical minerals cycle as a springboard for genuine industrial transformation, turning their underground wealth into the infrastructure and human capital that will sustain economic growth long after the current mineral cycle peaks.